There's a new shopper in your category. They don't browse. They don't respond to a well-placed end cap or a burst of color on your packaging. They ask a question, receive a recommendation, and move on. And increasingly, they're the ones making the call.

According to Boston Consulting Group's most recent research, generative AI now meaningfully influences up to 20% of consumer purchasing decisions globally. Salesforce tracked $67 billion in AI-influenced retail sales during Cyber Week 2025 alone. 20% of all orders processed across their network that week had a meaningful AI touchpoint in the journey. By 2030, analyst consensus puts agent-mediated retail spend well north of $100 billion.

These numbers are no longer projections. They are current reality. The question facing CPG brands isn't whether to prepare for the AI shopper. It's whether they're already too late to matter to one.

Not All Categories Are Equal

The urgency of that question varies enormously depending on where your brand competes. To sharpen the picture, we queried ChatGPT, Gemini, and Claude with the same structured prompts, then cross-referenced their outputs against published research from BCG, Salesforce, Capgemini, EY, and Bain. What emerged is a category-level view of where AI influence is actually concentrating, and where it's about to.

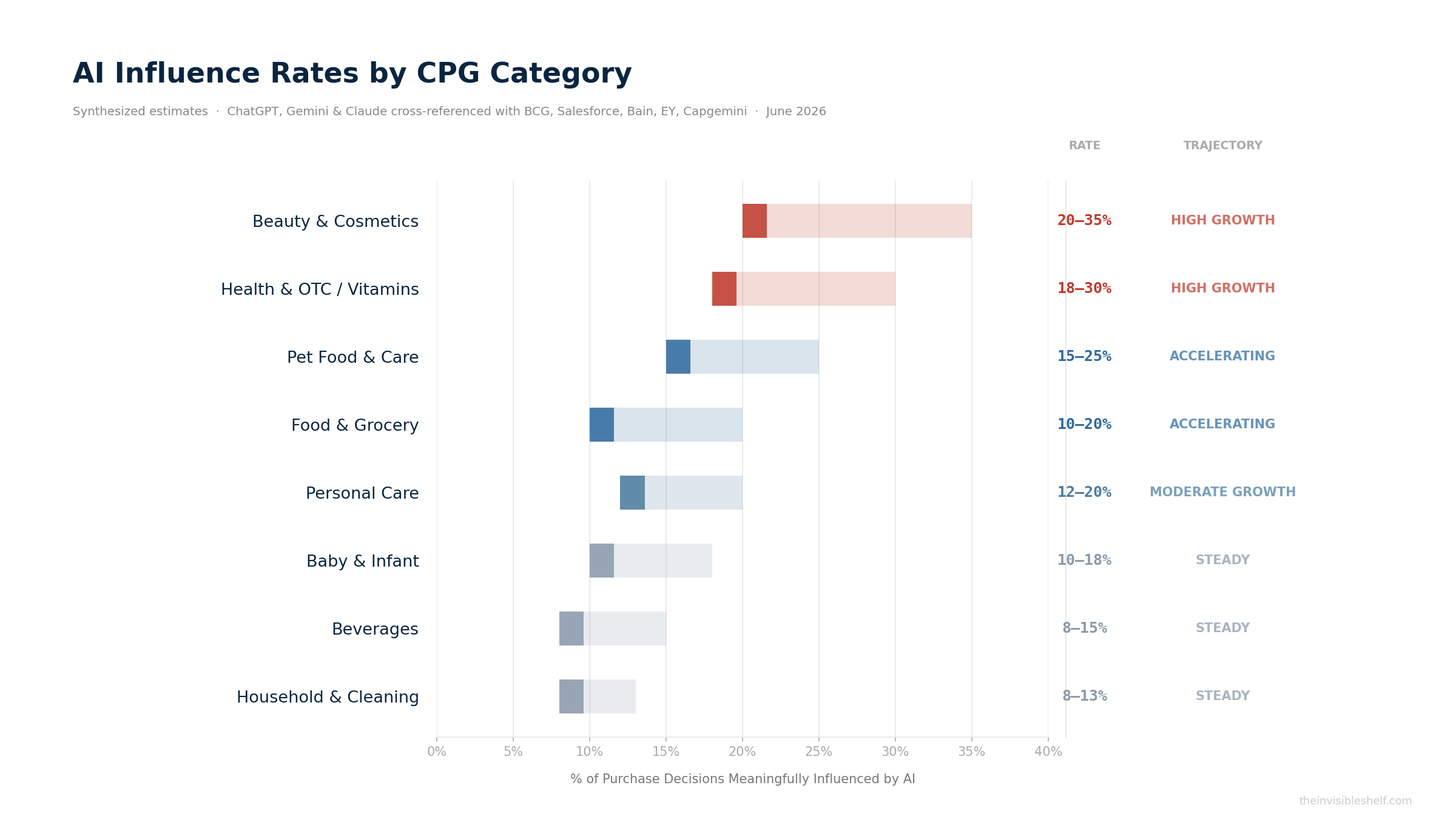

The divergence between models was itself a finding. More on that in a moment. But the synthesized view above shows current AI influence rates by CPG category, defined as the percentage of purchase decisions where AI meaningfully shapes the brand, item, quantity, or retailer selected. The range is wide. The trajectory divergence is wider.

Where AI Has Already Changed the Game

Beauty & Cosmetics sits at the top of the table for a reason. This is the category where AI has most successfully eliminated the friction that historically kept consumers uncertain: shade matching, skin-type compatibility, routine complexity. Virtual try-on tools, AR-coupled skin diagnostics, and conversational recommendation engines have collectively reduced purchase anxiety in ways that shelf design and packaging alone never could. Brands like Sephora and L'Oréal didn't stumble into this position. They invested deliberately in becoming AI-native at the point of discovery.

Health & OTC / Vitamins is the fastest-rising category in terms of trajectory. Consumers face what might be called supplement fatigue: an overwhelming volume of competing claims, ingredient lists, and format options. AI thrives in exactly this environment: high information complexity, high perceived consequence, and a consumer actively seeking to reduce cognitive load. The next wave will be driven by wearables integration. When your continuous glucose monitor or sleep tracker feeds directly into a supplement recommendation engine, the AI doesn't suggest. It prescribes.

Pet Food & Care may be the most underestimated category on the board. Pet humanization has been a trend for years; what's new is that consumers are now applying human-health-level research rigor to what they feed their animals. DTC-native brands like The Farmer's Dog are built AI-natively from the ground up: breed, weight, age, and health conditions map to individualized caloric profiles, updated continuously over the pet's lifetime. This is not a supplement to traditional CPG distribution. It is a structural replacement of it.

Where the Real Disruption Is Still Coming

Food & Grocery carries the widest variance between model estimates in our research: ChatGPT put it at 6–9%, Gemini at 25–30%. That gap is not noise. It reflects a genuine definitional split between digital and physical channel behavior. Most grocery trips still happen in a store, where AI influence is minimal. But the agentic commerce transition is likely to hit grocery harder and faster than any other category precisely because it is so habitual.

When an AI agent manages your weekly replenishment list (pulling from your purchase history, your dietary preferences, your pantry sensor data), the brand that wins is the one the algorithm recommends, not the one with the most shelf facings. BCG surfaces a pointed contradiction: grocery is currently the category where consumers are least likely to trust AI suggestions, yet it is also the category where the shift to AI-mediated agentic shopping will be most structurally transformative. Trust lags technology. It always does. Then it catches up fast.

The Model Divergence Problem

One of the more significant outputs of this research was the disagreement between AI models themselves. When queried on category-level influence estimates, ChatGPT produced conservative ranges (5–22% across all categories) while Gemini produced ranges two to three times higher (12–45%). Claude landed in between.

The gap comes down to definition. Gemini appears to count algorithmic ad-serving, social curation, and IoT-triggered auto-replenishment as meaningful AI influence. ChatGPT applies a narrower lens: direct conversational or recommendation-engine interaction at the moment of decision. Both are defensible. Both are real.

"The definitional ambiguity between models is not a research limitation to explain away. It is itself a strategic signal."

The Invisible Shelf

If you're a CPG brand trying to understand your exposure to AI-mediated commerce, the answer depends entirely on which AI touchpoints you're measuring. Most brands aren't measuring any of them.

Algorithmic Brand Equity: The New Competitive Moat

This research points toward a concept that deserves to become part of the industry's working vocabulary: Algorithmic Brand Equity (ABE): the degree to which your brand is structurally retrievable inside large language model recommendation architectures and agentic shopping ecosystems.

Traditional brand equity is built on awareness, affinity, and trust, measured through consumer panels and brand trackers. Algorithmic Brand Equity is built on something different: structured data quality, review density and sentiment, product description completeness, ingredient and attribute tagging, and LLM training data visibility.

The brands that built early digital shelf strength (strong PDPs, rich content, high review velocity) will have a head start. But the rules of the algorithmic shelf are not the same as the rules of the digital shelf, and that head start is not guaranteed to transfer. A brand can dominate search and still be functionally invisible to the AI recommendation layer. Many already are.

What This Means for CPG Brand Leaders

The 20% headline from BCG deserves to be stress-tested, not simply repeated. It is an average that masks enormous category variance: Beauty and Health/OTC are already at or above that figure and accelerating; Household Cleaning and Beverages are well below it. The strategic imperative is not to respond to the average. It's to understand where your category sits on the curve and how fast it's moving.

A few questions worth sitting with:

Is your brand optimized for the AI recommendation layer? Not just the algorithm, but the large language model. When a consumer asks an AI assistant to recommend the best moisturizer for combination skin, the cleanest protein bar under 200 calories, or the best senior dog food for joint health. Does your brand appear? Do you know?

Are you measuring AI-influenced conversion separately from standard digital attribution? If not, you are almost certainly misreading your own performance data. The shopper who asked Gemini for a recommendation before clicking your Amazon listing looks identical in your analytics. They are not identical in terms of what drove their decision.

Have you defined what "winning on the invisible shelf" means for your category? The brands that figure this out in the next 18 months will be extraordinarily difficult to displace. The ones that don't will spend the following decade trying to catch up.

The AI shopper is not coming. They're already in your category. The only question is whether your brand is ready to be found.

Sources: BCG (2026), Salesforce/Kantar CPG Leaders Survey, Capgemini GenAI Shopping Study, ALM Corp Consumer Study 2026, EY State of Consumer Products 2026, Bain Consumer Products Report 2025, eMarketer Agentic Commerce 2026. Cross-model AI queries (ChatGPT, Gemini, Claude) conducted live June 9, 2026.